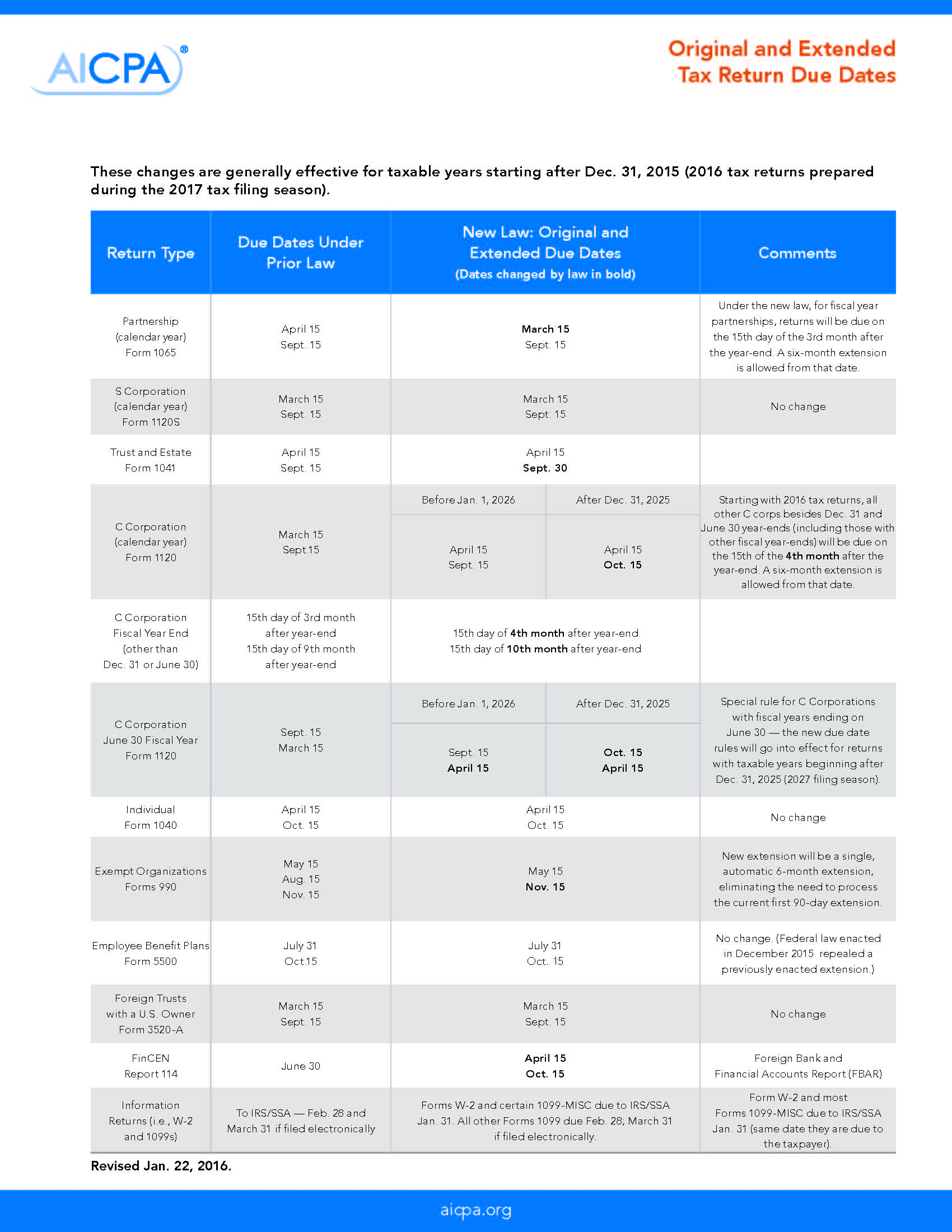

Extended Due Dates:

(These dates apply for taxable years beginning after Dec. 31, 2015 [2017 filing season — for 2016 tax returns]).

1. Forms 1040, 1065 and 1120S shall be a six-month period beginning on the due date for filing the return (without regard to any extensions).

2. Form 1041 shall be a 5½-month period beginning on the due date for filing the return (without regard to any extensions).

3. Form 1120 generally shall be a six-month period beginning on the due date for filing the return (without regard to any extensions). Note that Dec. 31 year-end C corporations before Jan. 1, 2026, shall have a five-month extension, and June 30 year-end C corporations before Jan 1, 2026, shall have a seven-month extension.

4. Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, for calendar year filers shall have due date of April 15, with maximum extension for a six-month period ending Oct. 15.

5. Form 3520–A, Annual Information Return of a Foreign Trust with a United States Owner, shall be the 15th day of the 3rd month after the close of the trust’s taxable year, and the maximum extension shall be a six-month period beginning on such day.

6. Forms 990 (series) returns of organizations exempt from income tax shall be an automatic six-month period beginning on the due date for filing the return (without regard to any extensions).

7. Form 4720 returns of excise taxes shall be an automatic six-month period beginning on the due date for filing the return (without regard to any extensions).

8. Form 5227 shall be an automatic six-month period beginning on the due date for filing the return (without regard to any extensions).

9. Form 6069 returns of excise taxes shall be an automatic six-month period beginning on the due date for filing the return (without regard to any extensions).

10. Form 8870 shall be an automatic six-month period beginning on the due date for filing the return (without regard to any extensions).

11. FinCEN Form 114, relating to Report of Foreign Bank and Financial Accounts, shall be April 15 with a maximum extension for a six-month period ending Oct. 15, and with provision for an extension under rules similar to the rules of 26 C.F.R. 1.6081–5. For any taxpayer required to file such form for the first time, the Secretary of the Treasury may waive any penalty for failure to timely request or file an extension.

Source: aicpa.org